Understanding the 2025 Social Security COLA Increase

The Social Security Cost of Living Adjustment (COLA) is an annual increase in benefits that helps protect retirees from inflation. The COLA is calculated based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which measures the average change in prices paid by urban wage earners and clerical workers for a basket of goods and services.

The COLA is designed to ensure that Social Security benefits keep pace with inflation, preserving the purchasing power of benefits over time.

Factors Influencing the COLA Calculation

The COLA is calculated using a specific formula that takes into account the change in the CPI-W from the third quarter of the previous year to the third quarter of the current year. The formula for calculating the COLA is:

(CPI-W for the third quarter of the current year – CPI-W for the third quarter of the previous year) / CPI-W for the third quarter of the previous year * 100 = COLA percentage.

For example, if the CPI-W for the third quarter of 2024 is 300 and the CPI-W for the third quarter of 2023 is 290, the COLA would be calculated as follows:

(300 – 290) / 290 * 100 = 3.45%.

This means that Social Security benefits would increase by 3.45% in 2025.

Historical Trends of COLA Increases

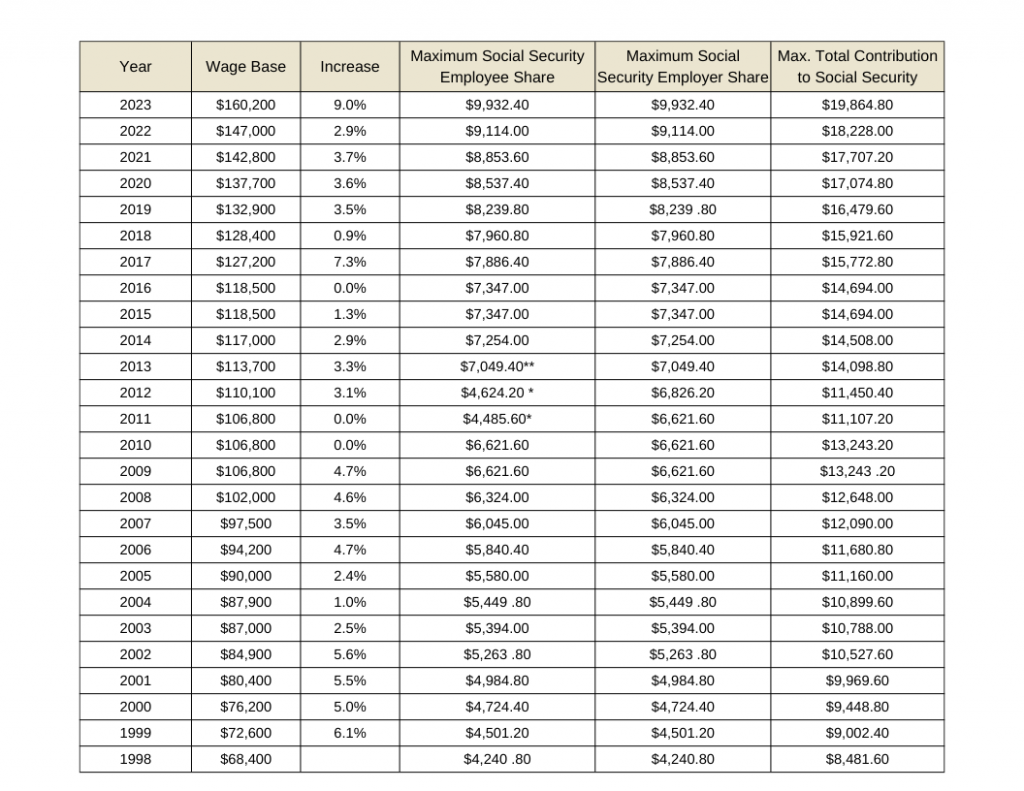

The COLA has varied significantly over the years, reflecting fluctuations in inflation. The average COLA increase over the past 50 years has been about 3.5%. However, there have been some years with much higher or lower COLA increases. For example, in 1980, the COLA was 14.3%, reflecting the high inflation of that period. In 2010, the COLA was only 0.3%, reflecting the low inflation of that period.

- 1980: The COLA was 14.3%, reflecting the high inflation of that period.

- 2010: The COLA was only 0.3%, reflecting the low inflation of that period.

Projected Inflation Rate for 2025 and its Impact on the Anticipated COLA Increase

The projected inflation rate for 2025 is expected to be around 3.0%. This means that the COLA for 2025 is likely to be in the range of 3.0%. However, it is important to note that these are just projections and the actual COLA increase may be higher or lower depending on the actual inflation rate in the third quarter of 2024.

Impact of the COLA Increase on Beneficiaries

The 2025 Social Security Cost-of-Living Adjustment (COLA) increase, while intended to help beneficiaries maintain their purchasing power, will have varying impacts depending on individual circumstances. The increase will affect the financial well-being of beneficiaries in different ways, depending on their income levels, expenses, and other factors.

Financial Implications for Different Beneficiary Groups, 2025 social security cola increase

The COLA increase will directly affect the amount of monthly Social Security benefits received by beneficiaries. However, the impact of this increase on their financial situation will vary based on their individual circumstances.

- Low-income beneficiaries: For individuals with lower incomes, the COLA increase will provide a more significant boost to their overall financial well-being. This increase could help cover essential expenses like food, housing, and healthcare, potentially alleviating financial strain.

- Higher-income beneficiaries: While the COLA increase will still provide a benefit to higher-income beneficiaries, its impact on their overall financial situation might be less pronounced. Their financial security may be less dependent on Social Security benefits, and the increase might be absorbed by higher expenses or offset by other sources of income.

- Beneficiaries with fixed expenses: Individuals with fixed expenses, such as mortgage payments or long-term care costs, might see a smaller impact from the COLA increase. The increase might not be sufficient to cover rising costs, leading to potential financial challenges.

Impact on Purchasing Power

The COLA increase aims to offset inflation and maintain the purchasing power of Social Security benefits. However, the effectiveness of this goal depends on the actual inflation rate and other economic factors.

- Inflation exceeding COLA: If inflation exceeds the COLA increase, beneficiaries might experience a decrease in their purchasing power. This means they might be able to buy fewer goods and services with their Social Security benefits despite the increase.

- COLA exceeding inflation: Conversely, if the COLA increase surpasses the inflation rate, beneficiaries might experience an increase in their purchasing power. They could potentially buy more goods and services with their benefits, improving their overall financial situation.

Challenges and Opportunities

The COLA increase presents both challenges and opportunities for beneficiaries.

- Potential challenges: The increase might not be enough to fully offset rising costs, particularly for individuals with fixed expenses. This could lead to financial strain and necessitate adjustments to spending habits.

- Potential opportunities: The increase could provide beneficiaries with additional financial flexibility, allowing them to pursue personal goals or improve their quality of life. This might include investing in their health, education, or leisure activities.

The Broader Context of Social Security in 2025

The 2025 Social Security Cost-of-Living Adjustment (COLA) reflects the ongoing challenges and complexities surrounding this vital program. While this increase offers immediate relief to beneficiaries, it’s essential to consider the broader context of Social Security’s long-term sustainability.

Historical Trends and Projections for Future Increases

Understanding the 2025 COLA increase necessitates examining historical trends and projections for future adjustments. The COLA is calculated based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which measures inflation in a basket of consumer goods and services. In recent years, the COLA has fluctuated, with significant increases in 2022 and 2023 due to elevated inflation rates. However, future COLA increases are projected to be more moderate, reflecting anticipated lower inflation rates.

Long-Term Challenges Facing Social Security

The Social Security program faces significant long-term challenges, primarily driven by demographic shifts and financial pressures. The aging of the baby boomer generation, coupled with declining birth rates, is creating a situation where fewer workers are supporting a growing number of retirees. This demographic shift, combined with rising healthcare costs and increased life expectancies, is putting pressure on the Social Security trust fund.

Potential Solutions to Ensure the Sustainability of Social Security

Addressing the long-term sustainability of Social Security requires a multifaceted approach that considers both revenue and expenditure adjustments. Potential solutions include:

| Solution | Description | Potential Impact |

|---|---|---|

| Raising the Retirement Age | Gradually increasing the full retirement age, allowing individuals to work longer and contribute to the system. | Increases revenue and reduces outlays, but may disproportionately impact lower-income workers. |

| Increasing the Social Security Tax Rate | Raising the payroll tax rate, increasing contributions from both employers and employees. | Increases revenue, but could discourage employment and economic growth. |

| Reducing Benefits | Adjusting benefit levels, potentially through means-testing or reducing the growth of benefits. | Reduces outlays, but may impact lower-income beneficiaries disproportionately. |

| Investing the Social Security Trust Fund | Allowing the trust fund to invest in a wider range of assets, potentially generating higher returns. | Increases potential returns, but also carries greater investment risk. |

| Expanding the Tax Base | Subjecting more income to the Social Security tax, potentially including higher earners or income from investments. | Increases revenue, but could face political challenges and potential economic impacts. |

2025 social security cola increase – The 2025 Social Security cost-of-living adjustment (COLA) will provide a much-needed lifeline for many Americans, but it’s important to remember that unexpected events can arise, demanding preparedness. Just as Northeast Ohio faces the challenges of emergency preparedness and response , we must be ready for life’s curveballs, ensuring that even with the increased benefits, we can weather any storm.

The 2025 COLA, while a welcome boost, should remind us of the importance of financial stability and resilience in the face of uncertainty.

The 2025 Social Security cost-of-living adjustment (COLA) is a reminder of the constant ebb and flow of life, much like the historical tensions between Iran and Israel, a conflict deeply rooted in ideology and geopolitics. Understanding the complex history of these tensions helps us grasp the fragility of peace and the importance of fostering dialogue and understanding.

The 2025 COLA, while a small step, symbolizes the ongoing effort to ensure the well-being of our citizens, just as global diplomacy strives to maintain stability in volatile regions.